The Molly & Claude Team Realtors Ottawa, Royal LePageTeam Realty

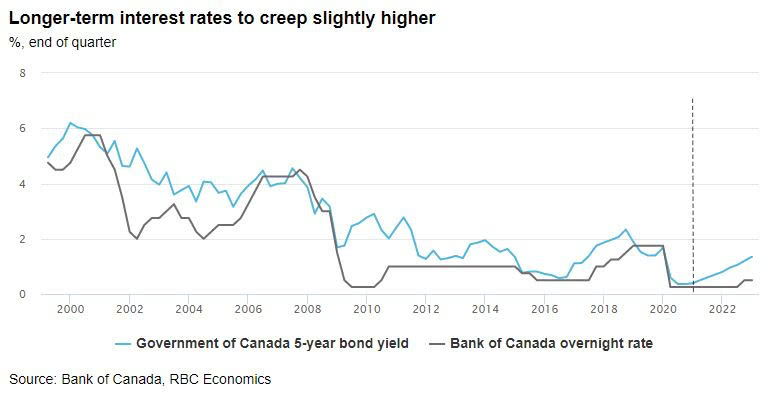

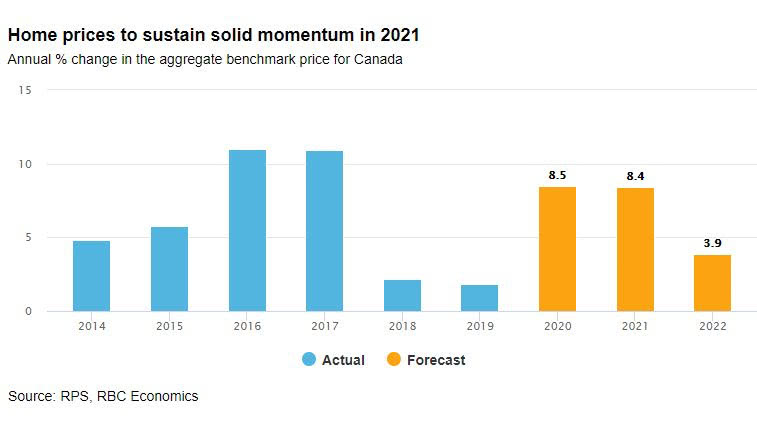

High sensitivity to interest rates poses a potential risk…

High sensitivity to interest rates poses a potential risk…