The June 6, 2024, news release from the Ottawa Real Estate Board (OREB) has garnered mixed reactions from various sources in the real estate community. Here are some of the key perspectives:

Market Stabilization: Many commentators noted signs of market stabilization. The increase in active listings and new inventory levels has been seen as a positive development, indicating a cooling from the previously overheated market. This is viewed as potentially beneficial for buyers who may find more options and less competition compared to earlier months.

Continued Price Increases: Despite the cooling, home prices continue to rise, albeit at a slower pace than before. The Ottawa market is still experiencing year-over-year price increases, which some believe could pose ongoing affordability challenges for buyers.

Balanced Market: Analysts and real estate professionals have pointed out that the increase in inventory and the moderation in price growth suggest the market may be moving towards a more balanced state. This could reduce the “multiple offer frenzy” that has characterized much of the recent market activity, providing a more stable environment for both buyers and sellers.

Reaction to Leadership Changes: The appointment of Nicole Christy as the new CEO of OREB has been positively received. Industry insiders are optimistic about her extensive experience and her potential to introduce new technologies and tools to support REALTORS® in the Ottawa area.

Cautious Optimism: While there is a cautious optimism about the future market trends, some experts urge monitoring over the summer to see if these trends continue. The current shifts are seen as a potential return to more typical seasonal patterns post-pandemic, which could signal a normalization of market dynamics.

Overall, the OREB’s news release reflects a market in transition, with signs of cooling but continued challenges related to affordability and inventory. The industry is watching closely to see how these trends develop in the coming months.

The number of homes sold through the MLS® System of the Ottawa Real Estate Board (OREB) totaled 1,545 units in May 2024. This was a decrease of 9.2% from May 2023.

Home sales were 3.7% below the five-year average and 13.2% below the 10-year average for the month of May.

On a year-to-date basis, home sales totaled 5,673 units over the first five months of the year — an increase of 5.2% from the same period in 2023.

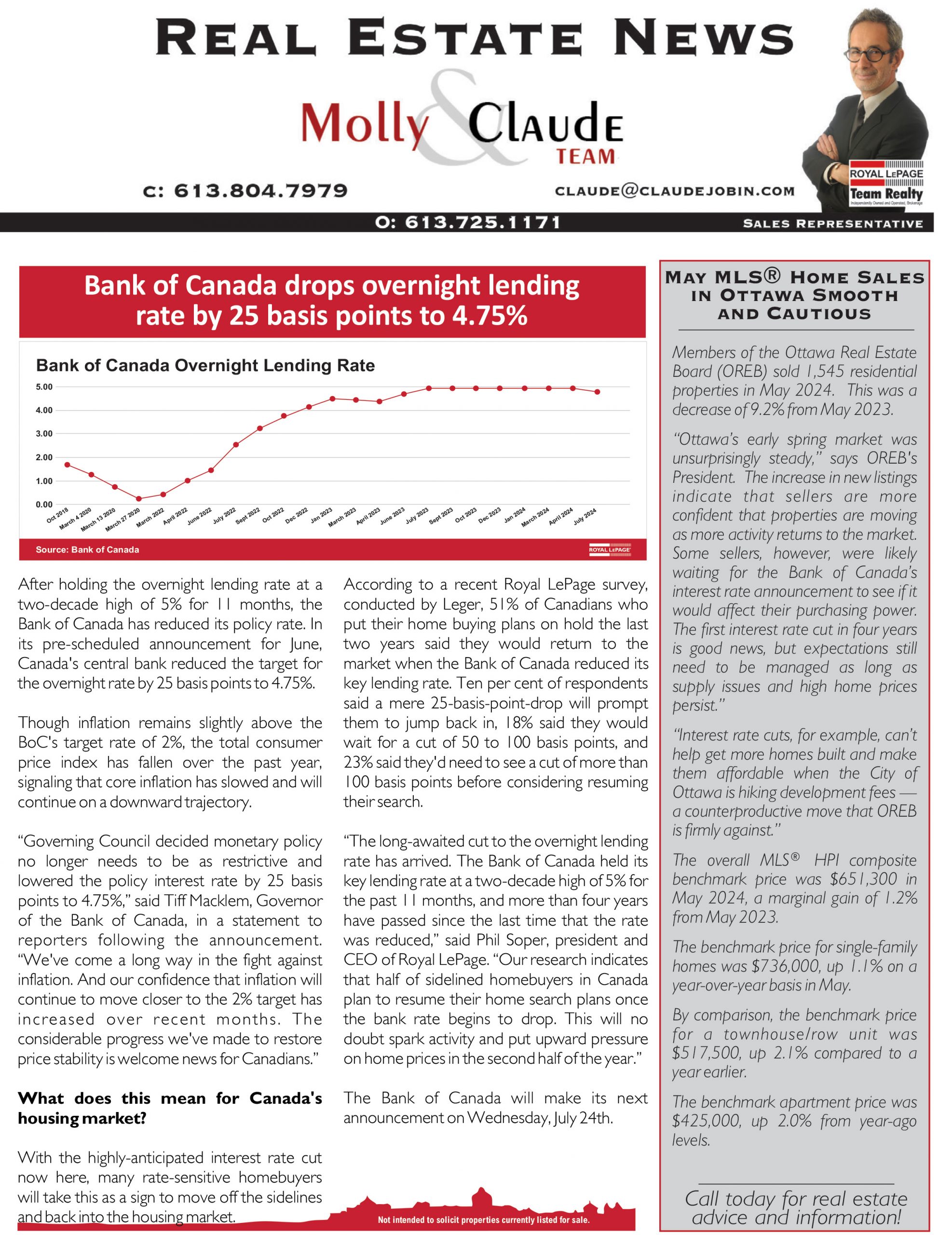

“Ottawa’s early spring market was unsurprisingly steady,” says OREB President Curtis Fillier. “The increase in new listings indicate that sellers are more confident that properties are moving as more activity returns to the market. Some sellers, however, were likely waiting for the Bank of Canada’s interest rate announcement to see if it would affect their purchasing power. The first interest rate cut in four years is good news, but expectations still need to be managed as long as supply issues and high home prices persist.”

“Interest rate cuts, for example, can’t help get more homes built and make them affordable when the City of Ottawa is hiking development fees — a counterproductive move that OREB is firmly against.”

By the Numbers – Prices:

The MLS® Home Price Index (HPI) tracks price trends far more accurately than is possible using average or median price measures.

The overall MLS® HPI composite benchmark price was $651,300 in May 2024, a marginal gain of 1.2% from May 2023.

The benchmark price for single-family homes was $736,000, up 1.1% on a year-over-year basis in May.

By comparison, the benchmark price for a townhouse/row unit was $517,500, up 2.1% compared to a year earlier.

The benchmark apartment price was $425,000, up 2.0% from year-ago levels.

The average price of homes sold in May 2024 was $690,683 increasing 0.8% from May 2023. The more comprehensive year-to-date average price was $679,862, increasing by 1.8% from the first five months of 2023.

The dollar volume of all home sales in May 2024 was $1.06 billion, down 8.5% from the same month in 2023.

OREB cautions that the average sale price can be useful in establishing trends over time but should not be used as an indicator that specific properties have increased or decreased in value. The calculation of the average sale price is based on the total dollar volume of all properties sold. Prices will vary from neighbourhood to neighbourhood.

By the Numbers – Inventory & New Listings

The number of new listings saw an increase of 26.2% from May 2023. There were 3,034 new residential listings in May 2024. New listings were 23.2% above the five-year average and 10.2% above the 10-year average for the month of May.

Active residential listings numbered 3,552 units on the market at the end of May 2024, a gain of 59.4% from May 2023. Active listings were 72.2% above the five-year average and 2.9% below the 10-year average for the month of May.

Months of inventory numbered 2.3 at the end of May 2024, up from 1.3 in May 2023. The number of months of inventory is the number of months it would take to sell current inventories at the current rate of sales activity.

More News from OREB

Welcome, Nicole Christy!

On June 3, 2024, OREB welcomed a new CEO, Nicole Christy. Nicole joins OREB from the London and St. Thomas Association of REALTORS® (LSTAR) where she rose to the position of Vice-President, Corporate Governance and Leadership Development.

“It’s a pivotal time in a rapidly evolving industry, but our mission remains steadfast: for OREB and its REALTOR® Members to be respected as the leading authority on real estate matters,” says Christy. “I know I’m joining an exceptional team and I look forward to working with everyone to bring our Members new tools and services that will elevate their practice and the value they offer to clients — including new technologies that facilitate barrier-free access to province-wide listing and property data.”

Nicole joined LSTAR in 2021 after several years working on housing policy and providing government relations support to some of Canada’s leading national associations, including the Canadian Real Estate Association (CREA), the Federation of Canadian Municipalities, and the Canadian Home Builders’ Association.

Swing and a hit!

Ottawa REALTORS® took to the greens on May 30, 2024, for OREB’s Annual Charity Golf Tournament, helping to raise an impressive $24,206.25. Through the Ontario REALTORS Care® Foundation, 100% of the funds raised will be donated to local shelter-related charities that provide a refuge, haven, or other type of protection from the effects of hunger, the elements, abuse, disabilities, and illness. In 2023, OREB donated more than $117,000 to local charities thanks to events such as the annual golf tournament and other fundraising initiatives.

On May 15, 2024 CMHC issued a news release pertaining to the April housing starts.

According to the Canada Mortgage and Housing Corporation (CMHC), the total monthly seasonally adjusted annual rate (SAAR) of housing starts for all areas in Canada decreased by 1% in April 2024, reaching 240,229 units compared to March’s 242,267 units1. The six-month trend in housing starts also declined by 2.2%, from 243,907 units in March to 238,585 units in April. Notably, the year-over-year decrease was driven by lower multi-unit starts (down 11%), while single-detached starts increased by 3%1. In major cities, Toronto experienced a 38% decline, Vancouver fell by 30%, and Montreal decreased by 3% compared to April of the previous year1. CMHC’s Chief Economist, Bob Dugan, attributed the multi-unit volatility to last year’s challenging borrowing conditions, particularly in Ontario1. For more detailed data, you can explore CMHC’s Monthly Housing Starts and Other Construction Data2

As of May 15, 2024, the Canadian Real Estate Association (CREA) reported significant activity in the Canadian housing market. National home sales surged by 11.3% month-over-month in April, continuing a trend of increased sales seen in previous months. Despite this surge, the actual number of transactions in April was 19.5% below April 2022 levels. The number of newly listed homes edged up by 1.6%, but new supply remains at a 20-year low, resulting in a sales-to-new listings ratio of 70.2%, well above the long-term average of 55.1%.

Home prices are also showing signs of recovery. The Aggregate Composite MLS® Home Price Index (HPI) climbed 1.6% from March to April, although it remains 12.3% below year-ago levels. The national average home price in April 2024 was $716,000, up $103,500 from January 2023, with significant gains seen in the Greater Toronto Area (GTA) and B.C. Lower Mainland.

The CREA attributes this market activity to pent-up demand, despite high interest rates, and notes that while new supply is gradually increasing, it remains insufficient to meet the strong demand.

The number of homes sold through the MLS® System of the Ottawa Real Estate Board (OREB) totaled 1,456 units in April 2024. This was an increase of 8.9% from April 2023.

Home sales were 2% below the five-year average and 6.9% below the 10-year average for the month of April.

On a year-to-date basis, home sales totaled 4,132 units over the first four months of the year — an increase of 11.5% from the same period in 2023.

“It’s a typical spring in Ottawa’s real estate market,” says OREB President Curtis Fillier. “What sets it apart from recent springs is a restored mutual confidence among both buyers and sellers. Buoyed by recent sales activity, sellers are more confident that they can move their property as evidenced by the uptick in listings. For buyers, the pressure of the pandemic market has eased and they’re comfortable taking the time to find the property that best suits their needs. The pace is still conservative while the economy is holding some back, but overall Ottawa’s market is strong and stable, and that’s a win-win.”

“The real story is in the details,” says Fillier. “Looking more closely at what’s selling and for how much suggests the demographic of buyer is changing. While most of Ottawa’s market is in balanced territory, townhomes have shifted to the seller’s market side as supply shrinks. Single-family homes are the most active market, which is inflating the average sale price. The next few months will be both telling and interesting as people continue to redefine their post-pandemic normal amid an upcoming federal election and back-to-work mandate for government workers. The detailed insights and data that REALTORS® have unique access to will be invaluable in helping buyers fine-tune their strategy for their specific neighbourhood and property type.”

By the Numbers – Prices:

The MLS® Home Price Index (HPI) tracks price trends far more accurately than is possible using average or median price measures.

The overall MLS® HPI composite benchmark price was $643,700 in April 2024, a marginal gain of 1.6% from April 2023.

The benchmark price for single-family homes was $727,700, up 1.6% on a year-over-year basis in April.

By comparison, the benchmark price for a townhouse/row unit was $500,800, up slightly at 1% compared to a year earlier.

The benchmark apartment price was $423,100, up 2.1% from year-ago levels.

The average price of homes sold in April 2024 was $705,117 increasing 1.2% from April 2023. The more comprehensive year-to-date average price was $675,817, increasing by 2.4% from the first four months of 2023.

The dollar volume of all home sales in April 2024 was $1.02 billion, up 10.2% from the same month in 2023.

OREB cautions that the average sale price can be useful in establishing trends over time but should not be used as an indicator that specific properties have increased or decreased in value. The calculation of the average sale price is based on the total dollar volume of all properties sold. Prices will vary from neighbourhood to neighbourhood.

By the Numbers – Inventory & New Listings

The number of new listings saw an increase of 40.5% from April 2023. There were 2,597 new residential listings in April 2024. New listings were 19.7% above the five-year average and 4.6% above the 10-year average for the month of April.

Active residential listings numbered 2,966 units on the market at the end of April 2024, a gain of 36.6% from April 2023. Active listings were 62.6% above the five-year average and 13.7% below the 10-year average for the month of April.

Months of inventory numbered 2 at the end of April 2024, up only slightly from 1.6 in April 2023. The number of months of inventory is the number of months it would take to sell current inventories at the current rate of sales activity.